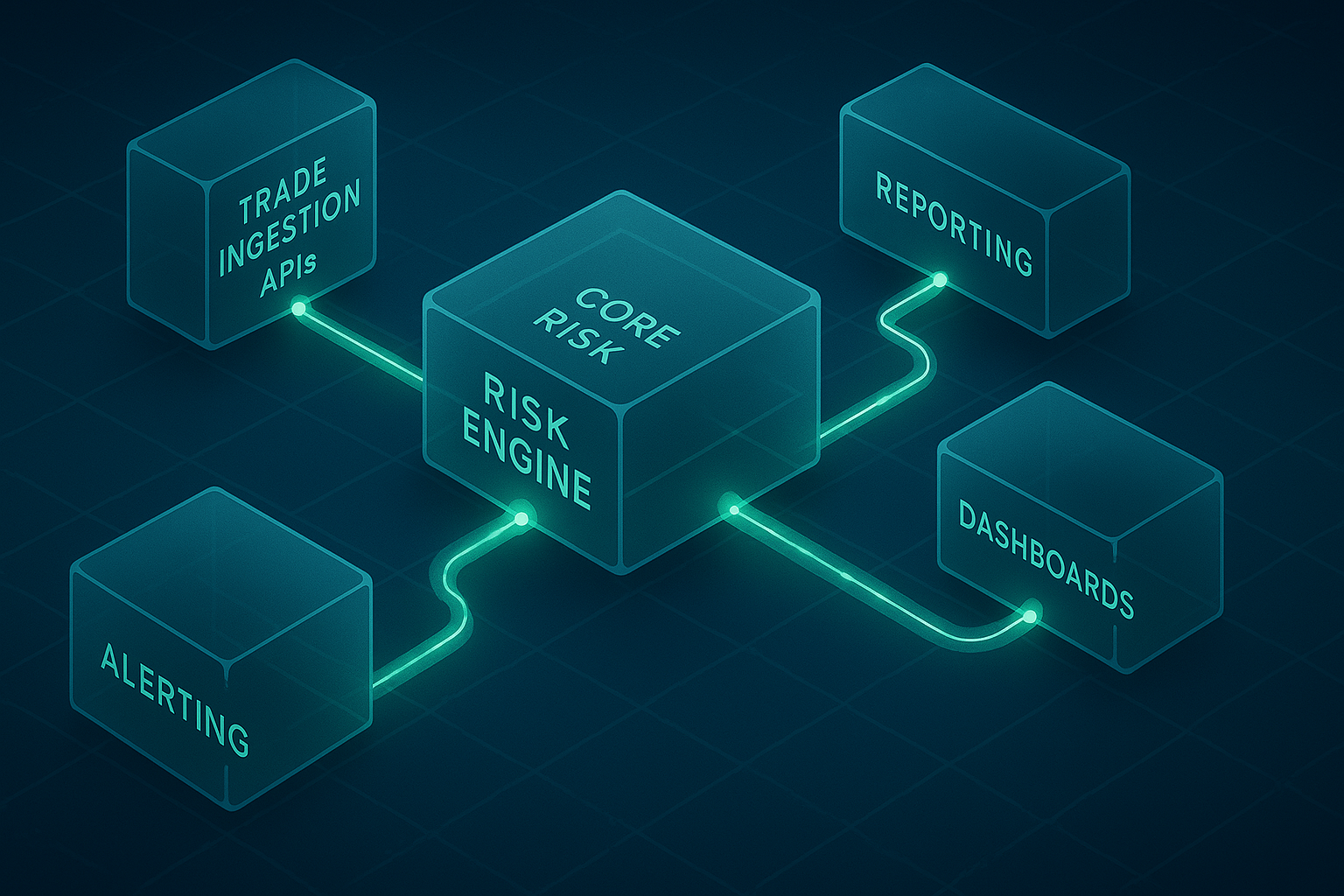

Clients, operators, and client AI enter through a stable API boundary and a first-party workbench. The platform resolves typed control objects, preserves evidence and artifacts, dispatches deterministic VRE jobs, and serves curated results through APIs, workbench views, BI, BigQuery, and regulator-ready packs.

Risk Architecture Flow Diagram Placeholder

(Visual: ingestion → AI mapping → deterministic kernel → results contract → delivery)

Channels & API boundary

Client systems, operators, and client AI enter through Apigee plus the Firebase-hosted workbench with typed northbound APIs and tenant-aware sessions.

Canonical control plane

Intake, scope, config, approvals, readiness, schedules, and resolved runs stay explicit as typed control objects with lifecycle and audit references.

Evidence & custody

Immutable artifacts live in Cloud Storage while canonical facts, evidence registries, and output load state are registered into BigQuery-backed product truth.

Dispatch backbone

Pub/Sub, Scheduler, and Tasks coordinate recurring schedules, retryable dispatch, downstream refresh, and operational decoupling across the platform.

Deterministic VRE runtime

GKE hosts the regulated compute plane: curves, pricing, XVA explain, sensitivities, stress, SIMM/DIMM, SA-CCR/SA-CVA/Market Risk, and governed evidence generation.

Serving, BI, and delivery

Serving views, low-latency projections, Looker dashboards, APIs, workbench cards, BigQuery access, and regulator-ready PDFs all consume curated facts instead of raw files.